As a fast-evolving industry, the market for woodland carbon continues to be influenced by passing, but significant, winds. As we have noted before, interest in the Woodland Carbon Code has expanded dramatically; demand for PIUs and WCUs has increased but the number of woodlands registered with the Code has been especially marked.

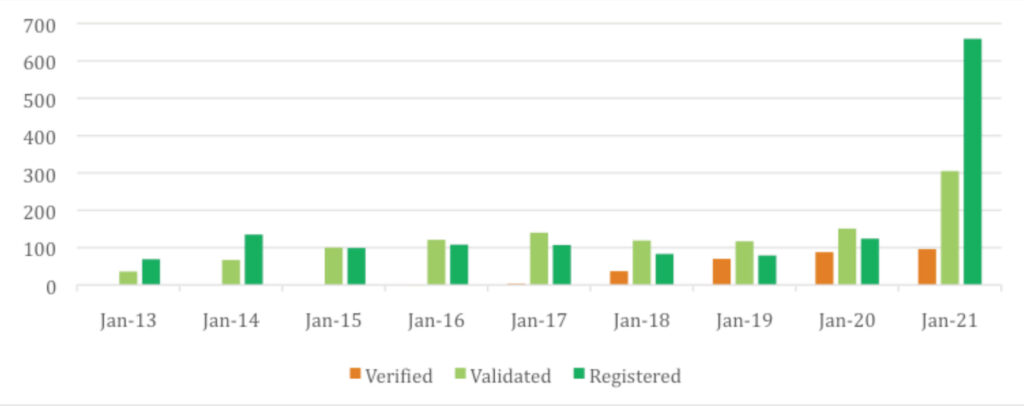

Chart 1: Number of Projects Registered with the Woodland Carbon Code (2013-2021).

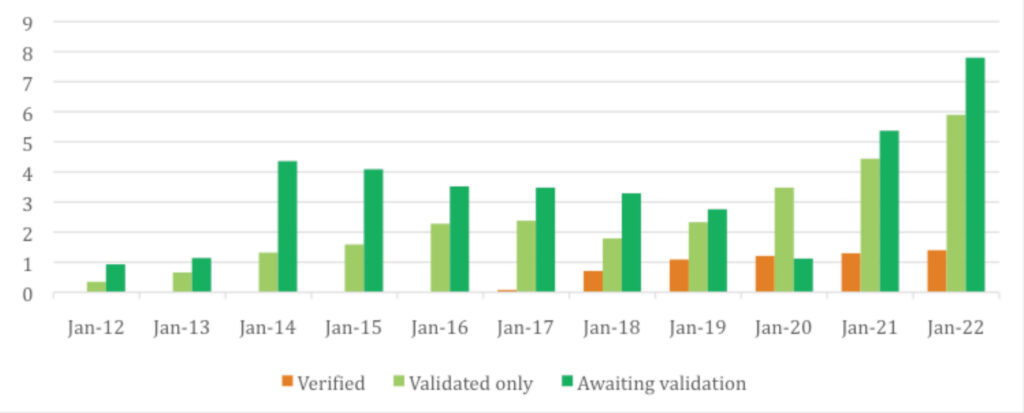

As chart 1 illustrates (see above), the number of schemes being registered with the Code rose over 5x year-on-year in the 12 months to January 2021. As a result, there are 7.8 million PIUs currently ‘awaiting validation’ (see chart 2 over the page) i.e. their projects have been registered but they are undergoing the various audits which are necessary before the PIUs can be issued on the UK Land Carbon Registry.

Chart 2: Projected carbon sequestration by Woodland Carbon Code projects in the UK (mn tonnes)

With these audits taking 4-6 months to complete there is a solid pipeline of supply building up along the system. Moreover, the Woodland Carbon Code allows projects to undergo validation within 3 years of being registered. It is a time-consuming process gathering the necessary documents so many of the registered projects are yet to submit themselves for validation.

Despite Long-Term Supply Growth, PIU Availability is Tight

In time, and with more schemes being registered each month (especially with the recently announced and valuable England Woodland Creation Offer now available), supplies of validated PIUs will increase. However, the long lead time between planting trees and receiving the PIUs is an important factor which is temporarily limiting supplies of validated PIUs. This is an important dynamic which, by limiting supplies, is influencing the price of PIUs. Prices are clearly rising. Recent conversations have revealed various pricing points. Woodland owners in Scotland are currently being offered between £8 and £10 per PIU by certain operators in the woodland market. Meantime, we understand that companies are being quoted between £15 and £20 per PIU.

This implies that certain ‘middle market brokers’ could be achieving a mark-up of over 100% on certain transactions. CarbonStore’s competitors appear to be making very substantial profits when they purchase PIUs from landowners. The transparent nature of CarbonStore’s business model means that we are able to offer landowner’s better prices for PIUs than our competitors and, for anyone contemplating the sale of their PIUs, a conversation with us is certainly in their best interests.

Encompassing the Wider Values of Natural Capital

Returning to the discussion on prices, we also understand that one recent entrant to the market is adopting a more holistic approach to valuing PIUs, attempting to combine the ecological, hydrological, and environmental values of their planting projects.

They also appear to be focused on larger-scale projects. As a result, they are offering quotes of £35 per PIU with a minimum order size of 30,000 units. This is an important and forward-looking effort to reflect the wider value of the natural capital growth from woodland creation. As is well known, woodland creation enhances the value of Natural Capital in many ways. For example, it improves water quality, it sequesters carbon, it prevents soil erosion and it amplifies biodiversity. Quantifying, valuing and amalgamating these assorted benefits is an essential step both for farmers and landowners to reap the full benefits of any planting schemes and for the government to reduce the high level of subsidies that are currently necessary to incentivise tree planting.

The Woodland Carbon Code Deliberates ‘Additionality’

The level of these incentives and the woodlands which should be eligible for carbon funding is a key deliberation for the Woodland Carbon Code right now. The combination of carbon funding and timber income, which the Woodland Carbon Code is enabling, is stimulating a significant upturn in planting interest across the UK.

However, the Code needs to distinguish between which of these woodlands would be getting planted anyway and which are reliant on carbon funding for their go-ahead. This distinction is central to the additionality test which is a core principle of all offsetting schemes globally; Would the carbon sequestering activity be occurring irrespective of carbon funding?

In practice, this is a very difficult question to answer. At the moment, major institutional investors are showing significant interest in the returns which, due to carbon funding, are now achievable from buying plantable land.

Carbon-related income, being realisable soon after planting and therefore not subject to the long wait and the heavy NPV-associated discount attributable to timber income, has transformed the investment potential of buying land with planting potential. Such projects are, therefore, inherently additional; They would not be occurring without carbon funding. However, the Woodland Carbon Code’s current proposals for the additionality test risk rendering many conifer- oriented schemes ineligible for carbon funding.

The Woodland Carbon Code as a Potential Force for Universal Good

As discussed earlier, interest in the Woodland Carbon Code has multiplied over the past 12 months. Indeed, by encouraging private sector companies to bear a meaningful portion of the costs of woodland creation while simultaneously providing the necessary financial incentives to landowners to plant trees, it could play the central role in achieving our ambitious planting targets.

If implemented carefully and judiciously, it could have many wider benefits. We could restore many of our landscapes to their native conditions, we could amplify the beauty and the wildlife of our countryside and we could vanquish our biodiversity crisis.

At the same time, we could also ensure sufficient resources exist to build our future homes in which timber, as the most sustainable building material available, will be a central component. Indeed, planting productive conifers is a key recommendation of the Committee for Climate Change who, in their January 2020 report, Land Use: Policies for a Net Zero UK, wrote:

“Sustainably managed forests are important for reducing emissions across the economy. They provide a store of carbon in the landscape and harvested wood can be used … as wood in construction, creating an additional stock of carbon in the built environment.” We must therefore tread carefully when deliberating additionality. The Woodland Carbon Code is rightly keen to maintain its credibility; Without that, the value of PIUs and WCUs will diminish. However, we must also realise that poorly designed policy could destabilise and discourage powerful but still incipient demand for planting. We will monitor developments closely on this.

Conclusion

The market continues to show classic symptoms of infancy. PIU prices are rising and optimism surrounding their continued ascent is high. Government policy is evolving rapidly: In England, generous planting grants have just been announced. Meantime, in Scotland, where similar policies have already proved successful, early signs of the reverse are emerging.

Options for landowners wishing to sell their PIUs are widening and, with CarbonStore’s growing success, they are no longer price takers, dependant on quotes issued to them by a duopolistic market. Instead, their PIU prices can be determined by supply and demand in the market.

Finally, the regulations governing carbon-oriented woodland creation are also changing. In June, the Woodland Carbon Code announced new rules for the timing of projects’ registration. They are now supplementing those by reassessing the criteria on which their eligibility for carbon funding is based. Please feel free to email me directly on david.mcculloch@carbonstoreuk.com if you have any questions regarding the above.

New Association formed to promote UK nature-based projects

Five of the UK’s leading developers of nature-based projects – including CarbonStore, part of Tilhill Forestry, have joined forces to form a new coalition. The UK Nature Projects Association (UKNPA) has been created to promote and accelerate woodland creation and peatland restoration schemes carried out to deliver climate and biodiversity benefits. A short film has […]

CarbonStore has produced this User Guide, so all parties have a clear understanding of the terminology and the processes involved in the selling and

purchasing of woodland generated carbon units.

Headline data suggests consolidation and stabilisation have characterised the market for woodland carbon in 2024

The UK Forest Market Report This article is from the 2024 edition of ‘The UK Forest Market Report’. The annual UK Forest Market Report (FMR) produced by Tilhill Forestry, provides an in-depth study of the UK commercial forestry and woodland investment market, from the perspective of both buyers and sellers. The 2024 report was produced in partnership with Goldcrest […]

Top Student Award for Evaluating Environmental Sustainability in its Third Year

A Graduate from Cranfield University has won the CarbonStore Top Student Award after achieving the highest mark on the ‘Evaluating Environmental Sustainability’ module within the Environmental Management for Business MSc.

Broadleaf Woodland Creation for Carbon Sequestration and Farm Diversification

Tilhill and CarbonStore, working closely with the landowner, designed and implemented the woodland creation plan, to help diversify the farm, sequester carbon and create community access.

Government to fund 180 local projects to boost water quality

£11.5m extra funding announced to boost tree planting, habitat restoration and flood management across England through the Water Environment Improvement Fund.

Webinar: Woodland Carbon – Unlocking an Increasingly Valuable Income Stream

Join CarbonStore for an informative webinar on 9th May 2024 to discuss the Woodland Carbon Code and the opportunities it offers farmers and landowners.

New housing developments to deliver nature boost in landmark move

In a world first, developers in England are now required to deliver 10% Biodiversity Net Gain when building new housing, industrial or commercial developments.

Innovation Zero is the UK’s largest net-zero congress, taking place on 30 April - 1 May 2024 at Olympia, London, to accelerate the transition towards a low carbon economy and society.

CarbonStore Prize Honours Excellence in Renewable Energy

A graduate from Edinburgh Napier University has won the CarbonStore Top Performing Student Award for the Renewable Energy Finance and Environmental Law module within the Renewable Energy MSc.

We are delighted to bring you a comprehensive guide on how businesses can offset their residual carbon emissions by harnessing the multiple benefits of planting trees in the UK.

A Carbon Source, Sink and Store: Explaining Soil Carbon

There is a lot of confusion surrounding terms such as ‘carbon sink’, ‘carbon store’ and ‘carbon source’. These three terms are neatly illustrated during a woodland’s life cycle.

UK among first countries to back new nature recovery fund

During the Global Environment Facility assembly in Canada, the UK announced it would stand among the first countries to contribute to the newly launched Global Biodiversity Framework Fund.

Thousands of trees to be planted in the UK to mark the Coronation

New £2.5 million tree planting fund to enable local authorities to create green spaces and connect communities with nature as a reminder of the Coronation.

AI to help UK industries cut carbon emissions on path to net zero

New artificial intelligence (AI) solutions will accelerate industrial decarbonisation across the country, with nearly £4 million in government funding for green innovations.

Podcast: Sustainable Forestry – Bringing the roots together

Heather Dinwoodie meets with David McCulloch, Head of CarbonStore at Tilhill, to discuss the challenges and opportunities of woodland creation and sustainable forest management.

The Business Case for Buying Woodland Carbon Credits

So, your business has calculated its carbon footprint, and reduced its emissions as much as possible, but what plans have you got in place to tackle your residual carbon emissions?

Top Student Award for Evaluating Environmental Sustainability

A Graduate from Cranfield University has won the CarbonStore Top Student Award after achieving the highest mark on the ‘Evaluating Environmental Sustainability’ module within the Environmental Management for Business MSc.

New investment in peat to help combat climate change

The government has announced new investment and actions to improve lowland peat and reduce carbon emissions, improving resilience to drought and supporting farmers.

Awards honor excellence in forestry and farming at the ‘Tree Oscars’

Farming and forestry were at the centre of the Scotland’s Finest Woods Awards 2023 with top honours going to a young farmer and a new commercial woodland.

Sustainable tree planting for carbon sequestration, biodiversity and timber production

Tilhill and CarbonStore, working closely with the landowner, designed and implemented the woodland creation plan, which was sympathetic to the landscape and offered many benefits to biodiversity.

Business Property Tax Relief for Woodland and Peatland Carbon Projects

The government’s consultation currently underway exploring the tax treatment of environmental land management and ecosystem service markets is therefore not only inevitable but long overdue.

Investment to boost community tree cover across parts of England

Projects will test new ways to increase tree cover and strengthen biosecurity, helping to mitigate the effects of climate change and meet the government’s 2050 net zero ambitions.

McLaren and CarbonStore unite to unpack a sustainable future

Port Glasgow based company McLaren Packaging has invested in planting a second Scottish woodland, removing 6,000 tonnes of carbon from the atmosphere through the duration of the project.

Farmers are central to food production and environmental action

Government speeds up Sustainable Farming Incentive roll-out with new sets of paid actions to support food production and environmentally responsible farming.

Webinar: Helping your business reach net zero through UK nature-based solutions

Has your business thought about planting home-grown trees in the UK to sequester your residual carbon emissions but you don’t know how to push the project forwards?

The Woodland Carbon Code can be complicated, but the development of the woodland carbon market also represents the evolution of a new and significant trend.

How restoring Wales’ bogs is improving water and wildfire security during dry weather

A new Natural Resources Wales report highlights how action to restore the degraded peatland of Wales accelerated at record pace during 2021/22 – even surpassing expectations.

New report analyses CO₂ uptake by different types of woodlands

A new report analysing CO₂ uptake by forestry shows that a diverse range of woodland types can all make a significant contribution over a 100 year period.

A Graduate from Cranfield University has won the CarbonStore Top Student Award after achieving the highest mark on the ‘Evaluating Environmental Sustainability’ module.

Woodland projects across England to receive funding for jobs, training and increasing tree cover

Funding will support projects which are expanding woodland cover, providing jobs and addressing the forestry sector’s skills shortage, and increasing access to nature

In practice, there are seven greenhouse gases (GHG) which the Kyoto Protocol identified as contributing to global warming. Carbon Dioxide (CO₂) is the most prevalent, accounting for 80% of GHG emissions.

Launched by the Forestry Commission in 2011, it is operated by Scottish Forestry, the science underpinning its calculations has been developed by Forest Research and it is backed by the UK government.

Delivering on the Environment Act: new targets announced and ambitious plans for nature recovery

New, long-term environmental targets have been announced by the government. The proposed targets are a cornerstone of the government’s Environment Act which passed into law in November last year.

BSW Sees More Trophies than Wood with Multiple Award Wins

BSW Group was presented with the Carbon Reduction Award (facilitated by CarbonStore) Selco pledged to plant over 100,000 trees across 100 acres at a site situated in the Scottish borders.

With the government legally committed to achieving net zero emissions in the UK by 2050 and simultaneously conscious of the wider societal challenges, its 2019 manifesto also committed it to planting 30,000 hectares across the UK by 2025

CarbonStore Sponsors Scotland’s Finest Woods Awards 2022 Climate Change Award

This exciting Award aims to celebrate leading examples of Scottish forests and woodlands, which have an important role in mitigating or adapting to climate change or sharing information or education.

Government unveils plans to restore 300,000 hectares of habitat across England

The new schemes will support nature recovery and climate action by rewarding farmers in their local area, alongside sustainable and profitable food production.

Scotland’s ‘Tree Oscars’ back with renewed climate focus

The premier awards for forests and woods in Scotland are back for 2022 after a highly successful 2021 saw winners ranging from a tiny nursery school to the country’s largest landowner

Productive Woodlands Must Play a Central Role in the Government’s Tree Planting Ambitions

Recent analysis by Forest Research, the Forestry Commission’s world-renowned research division, has highlighted an important shortcoming in the assumptions which underpin the current approach in calculating sequestration volumes by different types of woodland

Mental health benefits of visiting UK Woodland’s estimated at £185 million

Visits to the UK’s woodlands boosts mental health and is estimated to save £185 million in treatment costs annually, a landmark report published by Forest Research finds

CarbonStore is delighted to welcome Michael Fagbohungbe to both the Tilhill and CarbonStore team. His appointment means that the Company can really dig deep into the business of carbon, starting by assessing its own ambitions towards Net Zero as well as reinforcing the CarbonStore team by providing his expert knowledge in carbon offsetting. Michael holds […]

New Report Examines Bog Breathing to Monitor Peatland Restoration

The report released on #BogDay used satellite technology to look at how these bogs breathe" and how it could help build a better picture of peatland conditions in Scotland.

Carbon sequestration describes the process in which carbon dioxide (CO₂) is removed from the atmosphere and subsequently stored through biological, chemical, or physical processes.

Fourth Woodland Carbon Guarantee auction dates announced

£10m available from the scheme’s £50m pot for farmers and land managers to create new woodlands to help tackle the effects of climate change. The scheme gives land managers the option to sell Woodland Carbon Units (the carbon captured once the trees have grown), to the government at a guaranteed price protected against inflation. The […]

Creating Woodlands For Cash, Carbon and Conservation in England

Head of CarbonStore David McCulloch Joins Panel Free Webinar: Tuesday June 22nd – 11am Tilhill, the UK’s leading forestry management company announces the latest in a series of free webinars. The webinar on 22 June will focus on exploring the new funding offer for woodland creation in England. The webinar will take farmers, landowners and […]

We see signs of infancy across all carbon markets, including the one for woodland carbon. The absence of pricing transparency, which we are keen to rectify, is the most obvious symptom. Meantime, we continue to work hard to address others which we feel are important steps to ensure the healthy development of the market so […]

FCCWG Webinar -The Importance of Carbon in a Climate Emergency

The Forestry & Climate Change Working Group with CarbonStore The Forestry Climate Change Working Group (FCCWG) present this Workshop Webinar; a free online workshop for forestry practitioners exploring the importance of carbon in a climate emergency. As a result of the UK’s commitment to becoming a Net Zero economy by 2050, carbon sequestration is likely […]

The outlook for the woodland carbon market appears encouraging. Its regulatory standard, the Woodland Carbon Code, has used the lockdown gainfully to update its rules and guidelines, expand its capacity and widen its recognition among both landowners and companies. With the UK now (slowly) emerging from the lockdown, pressure for a ‘green recovery’ is growing. […]

Creating Woodlands for Cash, Carbon & Conservation Webinar

Head of CarbonStore David McCulloch joined Tilhill for this informative webinar entitled ‘Creating Woodlands for Cash, Carbon & Conservation’ – Scotland which included three onsite interviews. David answered all carbon related questions from landowners, farmers and industry professionals. Watch the full recording covering: The landowner’s objectives Evaluating the land and farm potential How agriculture can […]

Free workshop: Tuesday 20th April 11am The Forestry Climate Change Working Group is delighted to announce the launch of a free online workshop for forestry practitioners and will explore the importance of carbon in a climate emergency. As a result of the UK’s commitment to becoming a Net Zero economy by 2050, carbon sequestration is […]

The UK’s woodland carbon market is evolving rapidly. Preliminary enquiries, more substantive indications of interest in buying PIUs, and firm orders for them from companies have all picked up markedly through January and early- February. Similarly, woodland owners are quickly recognising the opportunities from selling their woodland-generated carbon credits. The number of schemes being registered […]

World Wetlands Day – Restoring a globally important habitat

Forestry and Land Scotland’s (FLS) ongoing work to restore a globally important habitat is being celebrated as part of World Wetlands Day (2 Feb). Blanket bog is a type of habitat found on peatland soils in cool, wet upland areas in maritime climates. It covers 23 per cent of Scotland’s land area and is rarely […]

The business of net-zero: Natural climate solutions – CLA Podcast

Listen to CLA’s podcast supported by Tilhill. ‘David Attenborough’s recent Netflix documentary did an incredible job making the case that the key to solving climate change is right in front of us: nature. Nature is our biggest ally, inspiration and the best, most cost-effective, shovel-ready technology we have to tackle the climate crisis.’ In this podcast we focus on […]

CarbonStore Sponsor 2021 Tree Oscars to reward Climate Change Champion

A new Climate Change Champion prize has been added to Scotland’s Finest Woods Awards as the ‘Tree Oscars’ return in 2021. The Climate Change Champion Award, sponsored by CarbonStore, will be chosen by judges from entries to all 2021 Awards categories. All entries can identify and highlight what their project will contribute to tackling climate […]

The Benefits of Nature-Based Solutions for Your Company and Its Environmental Goals

Webinar: Crafting Nature-Based Solutions for Your Business January 28th 10am What are nature-based solutions? How can they help your organisation? How do they work, in practice? CarbonStore is well equipped to explain. Through Tilhill, we have 70 years’ experience in planting trees and restoring peatlands. Please join us for our free webinar discussing these issues […]

Green carbon initiatives join forces to expand the UK market

In the race to tackle climate change and to reach net zero emissions, two key UK-wide carbon markets have joined forces. The UK Woodland Carbon Registry and UK Peatland Code have come together to form the new UK Land Carbon Registry. The new registry aims to create a more accessible ‘one-stop-shop’ for woodland and peatland […]

CarbonStore and The Woodland Carbon Code – Webinar Recording

CarbonStore, a company providing an open and transparent platform for companies and landowners to buy and sell Woodland Carbon Units is delighted to share this free public webinar dedicated to farmers, landowners and companies. The online event on November 3rd 2020 introduced CarbonStore and outlined the Woodland Carbon Code. The webinar attracted over 240 guests […]

When considering environmental enhancement, it can sometimes feel as though there are too many variables to juggle or prioritise to make the most significant impact possible with the resources at your disposal.

The intricacies of the Woodland Carbon Code present many potential pitfalls for landowners seeking to capitalise on their newly planted woodland’s carbon sequestration capacity.

An Insight into Current Prices of Woodland Carbon Units

We market our carbon-related woodland schemes fairly and openly and we charge only a minor commission for arranging the transactions between landowners and companies.

A Unique Carbon-Offsetting Business Launches Today

A new opportunity launches today for those of us seeking to contribute to a cleaner, greener, low carbon economy. CarbonStore will be utilising its unique partnerships to unite landowners, who are looking to sell woodland generated carbon units, with companies that are keen to offset their carbon emissions. The objective being to provide a woodland-based […]

The report assesses the way we use our land today and the changes required in how we farm and use land in order to deliver the UK Government’s Net Zero greenhouse gas emissions target by 2050

Reducing UK emissions: 2020 Progress Report to Parliament

This is the Committee’s 2020 report to Parliament, assessing progress in reducing UK emissions over the past year. This year, the report includes new advice to the UK Government on securing a green and resilient recovery following the COVID-19 pandemic.

UK Woodland Creation in the Past 12 Months: We Still Have a Lot To Do…

On 11th June, the Forestry Commission gave us our annual insight into tree planting volumes across England, Scotland, Wales and Northern Ireland for the 12 months from 1st April 2019 to 31st March 2020.

Third Woodland Carbon Guarantee auction now open for applications

Some great news for landowners in England looking to bid on an earlier than expected third auction with the WCaG, with some interesting results from the second auction from June 2020.

Pending Issuance Unit: A promise to deliver a Woodland Carbon Unit during a given period, based on the trees’ predicted growth

Woodland Carbon Unit: A ton of carbon dioxide which has been sequestered in a scheme verified under the Woodland Carbon Code